We are glad to have gained perspective on investing during a period of potentially transformative new technology since investors did not fare well for extended periods in pervious episodes. Much of our perspective was gained from Alistair Nairn’s great book, “Engines That Drive Markets”. The phrase above is excerpted from that book.

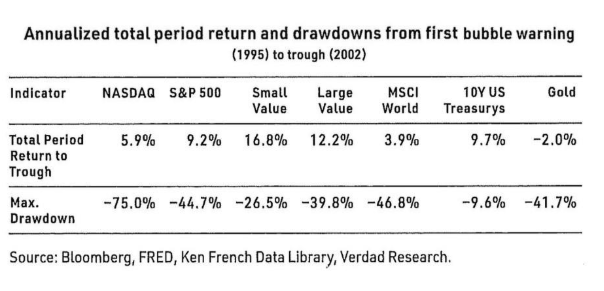

Internet Boom – Well respected investors including Warren Buffett, Seth Klarman, and others were warning about excessive market valuations during the dotcom period as early as 1995, well before the bust. We expressed the same views. For years they appeared to be wrong as the Nasdaq 100 returned an amazing 40% per year from 1995-1999. Ultimately, their shareholders benefited from their advice when the bubble burst in 2000.

Despite looking wrong for a long time and using a 1995 start date, you can see that investors fared much better by investing in stocks that weren’t caught up in the excesses of the internet during that period.

The internet clearly transformed large chunks of the economy and made them more efficient, but it wasn’t until the middle of the decade that companies like Apple, Facebook, Google, and Amazon started to profit greatly from the new technology.

The Nasdaq 100 has returned 19% per year for the last 5 and 10 years which is not as extreme as returns leading to dot-combust, but we think investors should still be mindful that it took the Nasdaq until April 23, 2015, fifteen years later, to reclaim its 2000 high during the peak of the dotcom boom. It took until 2013 for the S&P 500 to reclaim its 2000 high on a sustained basis and the telecom sector, the epicenter of the excessive buildout of the internet, remained 40% below its 2000 peak as late as 2017.

For the decade after the 2000 peak, the S&P 500 and Nasdaq suffered negative annual returns of (2.75%) and (6.40% ), respectively. Poor returns and similar trends were seen in previous technology related booms as discussed later.

Cisco Systems is an example of how investors can get burned by a bubble as it went through a process reminiscent of past bubbles. Investors would have done well investing in Cisco Systems at the IPO in 1990 when they were receiving a risk premium. But by 2000 investors were receiving no risk premium they were buying euphoria. At $77 recently, Cisco is still below its adjusted peak of $80.06.

They were a dominant intranet infrastructure stock in 2000 with rapidly rising sales and earnings, but they then went through a reckoning typical of technology companies where once penetration increases (fewer people need routers) pricing becomes important to selling products. Sales started to flatten and margins were under pressure. As in earlier technology bubbles, investors were simply not factoring in that likely process in 2000.

The companies that ended up benefitting the most from the Internet were not the infrastructure providers at the top of the market during the 2000 bubble, investors in those companies didn’t fare well, but investing years later in the companies that commercialized the internet effectively proved very rewarding. But sustained stock gains for those companies, Amazon, Google, Facebook and Apple didn’t take place until 2008 for Amazon and Google and Facebook didn’t come public until 2012, well after investors made and then lost money during the bubble.

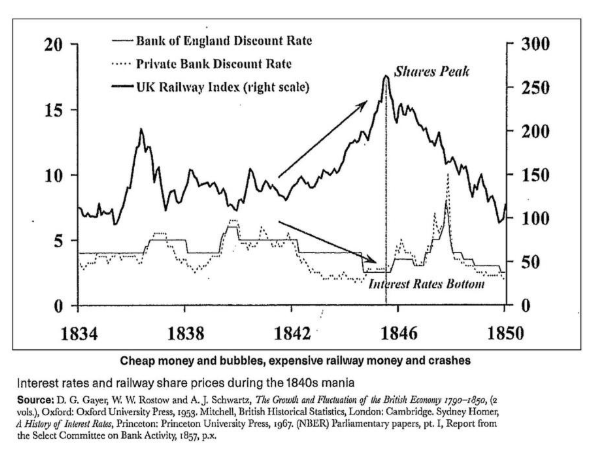

The Industrial Revolution was one of the most important technological breakthroughs of the modern era and the driving force in economic expansion in Europe and the U. S. during much of the 19th century. Mass production enabled by the new machinery led by the steam engine drove down the cost of many new items previously made meticulously by skilled craftsmen. Larger quantities of goods at lower prices in the industrial centers also led to the need for the railroads to move the goods from the urban centers where they were made to end markets across the country. Much like today the new technology was very capital intensive.

Any technology that requires high capital investment and a long period of earning profits to cover those costs is a high risk undertaking unless there is some form of protection against competition, particularly if it is subject to obsolescence. Canals are an example as they lowered the cost of transportation transforming the industry, but the large upfront costs were not profitably recouped because of the introduction of the railroads who could ship goods for at least one third less than the canals.

Railroads also took much longer to cover their capital costs and enjoy sustained profitability than early investor enthusiasm seemed to anticipate. Sustained profitability didn’t happen for years and only after the industry consolidated by reducing excess lines which were built as investors rushed to make big gains.

Despite early safety problems, the advance of the railroads was unstoppable, and the technology quickly proven but introduction in Britain required land to be purchased and buildings to be torn down to make room for tracks.

George Hudson of Hudson Railways gained control of 25% of England’s railroads. His access to large amounts of capital was fueled by paying a large dividend despite not earning it since he artificially lowered expenses to show a profit. He also purchased newspapers to promote his popularity.

This promotional environment persistently shows up in the early stages of a new technology and is a necessity to raise funds and represents a risk to investors. All joint stock companies of the period required government approval, so Hudson helped one of his supporters get elected to parliament.

Attracted by a bull market, low interest rates, and the irresistible appeal of the financial press groups of folks never known to the Stock Exchange rushed to place their small savings often on margin.

The boom finally ran out of steam in the 1840’s. Interest rates rose due to the potato famine as outflows of bullion to pay for potato imports forced interest rates higher. Higher interest rates or a worsening economic environment have repeatedly provided a reality check to overly optimistic investors particularly during periods of technological breakthroughs. That’s typically when reality sets in. Hudson was exposed as a crook who had produced fraudulent accounts to bolster profitability and allowed dividends to be paid out of capital.

Investors driven by visions of large profit lost sight of considering whether revenues would exceed expenses when reviewing new railway lines. Nearly 20% of the track authorized for construction in the U. S. was abandoned as were fiber optic lines during the dotcom boom.

Remaining companies tried to rebuild profitability through a series of combinations. Currently, there is a similar race by many companies to dominate AI and it appears profitability won’t be a priority until the race is over. Based on prior historical episodes, increased profitability is not likely to happen until the industry consolidates.

In the 50 years after the railway bubble burst from overheated expectations and changing economic times investing in railways was not rewarded in absolute or relative terms as seen below.

Electric Lights

The demand for whale oil hunted whales in the Atlantic Ocean out of existence. Getting supply from the Pacific drove the cost of whale oil to $2.50 a gallon almost $400 a gallon in today’s terms. That paved the way for coal gas and kerosene refined from the oil fields in Pennsylvania to take whale oil’s place. It took forty years for electricity to replace kerosene and coal gas.

Coal gas was structured as a monopoly because of otherwise prohibitive upfront infrastructure costs. This led to complacency, higher costs and the resulting consumer resentment led to replacement technology. Early development of electric lights was a battle between arc lighting and incandescent lamps with arc lighting originally thought to be the winning technology.

From 1856-1870 lighthouses in Britain were fitted with carbon arc lighting. Arc lighting was originally seen as the technology leader but ultimately lost out to incandescent lamps as it was held back by the prohibitive cost of batteries and noxious fumes produced by combusting carbon.

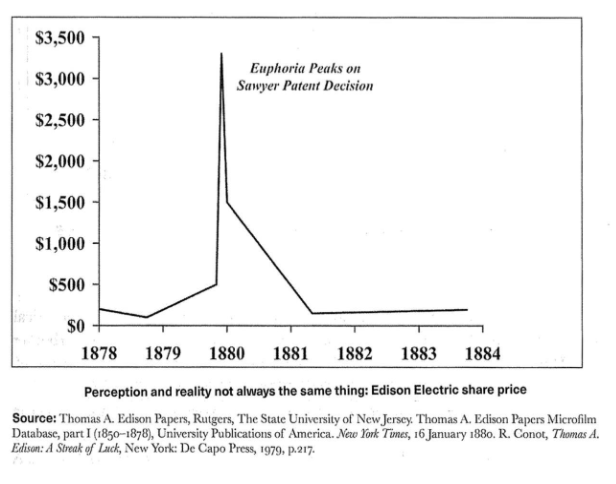

The first product that was truly better was Jablochkoff candles, but they were much more expensive. So, Charles Brush started the Anglo-American Brush Electric Light Company using Arc lighting . During the euphoria over this new technology , the Brush company went up seven times and the Hammond company 4 times but 12 months later the bubble burst when it was apparent Arc lighting could not compete cost wise with coal gas to produce lighting and the bubble burst. The Arc light companies dropped from sight either being liquidated or bought up by incandescent lamp companies.

Thomas Edison was one of the leaders in incandescent lamps and was approached in 1876 by Cornelius Vanderbilt to invest in his company. Ultimately GE was started in 1894 to much success but only after Edison battled with Westinghouse whose alternating current technology ultimately supplanted direct current which Edison originally thought was the best technology.

After losing a patent dispute with William Sawyer (which he ultimately won in 1880) and battling with alternating current, Edison needed to merge his electric companies into one company and then merge with Thompson Houston ,a top competitor. To strengthen his financial position. The battle to supply the country with electric light took decades not months until GE and Westinghouse finally won out but prior to GE being formed in 1894 the price of Edison’s electric company struggled for many years.

THINGS TO CONSIDER IN THE CURRENT ENVIRONMENT

General optimism and historical high valuations which exist today are in large part because it’s been 16 years since investors sustained losses and those memories have faded away.

After bubbles burst, the economy can also suffer in the medium term as capital gets destroyed and consumption suffers as savings go up to repair the stock of available capital

Henry Ford had two car companies go bankrupt before his third venture Ford Motor Company was successful.

After the internet bust, the recession in 2000 was mild because the Federal Reserve dropped rates to 1% and the Federal government went from running surpluses to a federal deficit of 5%, equivalent to a 5.5% stimulus to the economy. With our current debt situation and inflation remaining elevated near 3%, federal authorities are in a much weaker position to be support the economy

Technology can change the world, but it can’t change human nature as seems evident in the repeated patterns that occurred previously. We are reluctant to invest in AI since our expectation is that as it matures a sense of reality will set in.

CONCLUSIONS

The current period feels similar to the dotcom period to us. Despite not yet quite reaching the same level of dangerous excess, we think investors are too caught up in the potential to make large sums of money in a short period of time and are overly complacent about the risks. This pattern has been repeated historically during markets that were heavily influenced by a significant technological breakthrough. Both the Nasdaq 100 and the S&P 500 are highly concentrated in AI related stocks and vulnerable to a period similar to the post internet bust period.

Internet technology clearly worked as did railroads and electric lights, but early investors still suffered from excessive hype and the shifting sands in the winning technology. Despite its potential, doubt remains about the economic value of AI which is not reflected in their valuations in our view. We also believe high valuations for AI related stocks fails to consider the potential pitfalls a review of past technological breakthroughs suggests.

According to Nairn , in the early stages of a breakthrough technology, there’s a battle between the cash burn rate and the retention of investor confidence. Obviously, this doesn’t apply to financially strong big tech companies, but it certainly applies to their customers. A review of such episodes in the past suggests failure will often be the case. That doesn’t agree with our idea of seeking a margin of safety in our investments. The history of technological advances suggests a cautious approach.

Finally, our view is investors without a specialist’s knowledge of the technology should display a high degree of caution given the high risk of failure particularly if the new technology comes to the public during a benign economic period more prone to speculation and excess capacity.

This article is an excerpt from our most recent Newsletter. If you are interested in receiving our newsletters, please feel free to click here: Sign up

We will be hosting a presentation at Cape Fear Country Club regarding this article topic from 5-7 on February 25th to discuss our investment philosophy and view of the current environment. Beth Boney Jenkins will also be speaking. Beth is the development officer for the North Carolina Community Foundation in the eastern part of the state. Beth is a Chartered Advisor in Philanthropy and well versed in effectively collaborating with donors and their advisers on legacy planning. We would love for you to join us. You can reserve a spot by emailing us at [email protected].

Investment advisory services offered through South Atlantic Capital Management Group, Inc., a registered investment advisor. The information published herein is provided for informational purposes only, and does not constitute an offer, solicitation or recommendation to sell or an offer to buy securities, investment products or investment advisory services. Illustrations are for presentation purposes only. Actual investment experience will vary with investment selection and changing market conditions.

LINC Inc. Welcomes Four New Board Members

Staff Reports

-

Aug 4, 2026

|

|

Novant Health Acquires Wilmington Surgical Associates

Cierra Noffke

-

Aug 4, 2026

|

|

Legal Aid Of North Carolina To Relocate Wilmington Office

Cierra Noffke

-

Aug 3, 2026

|

|

Wellness Destination Slated For Former Lowe's Foods Site

Emma Dill

-

Aug 4, 2026

|

|

DiSisto Tapped As Executive Director Of BCC Foundation

Staff Reports

-

Aug 4, 2026

|

|

After working as an instructor for others, he opted to work for himself and is the owner of Fred Astaire Dance Studios locations in Wilmingt...

Wilmington's live music scene includes a mix of options and genres, but also faces challenges....

"Mayfaire has evolved into one of the most important commercial submarkets in Southeastern North Carolina because it offers a combination th...

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.