In our view, taking money out of your best ideas—where you have the most confidence in future returns and ability to withstand risks—to put it in companies you know less about and have less confidence in makes little sense.

Legendary investor, Philip Fisher, who has one of the best long-term track records said it this way many years ago:

“Investors have been so oversold on diversification that only a small percentage of their holdings are in attractive stocks that they know much about. It never seems to occur to them that buying a company without having sufficient knowledge may be even more dangerous than having inadequate diversification.”

For the equity portion of portfolios, we have found that 15-25 well-selected companies provides adequate diversification and that our knowledge level of the companies in the portfolio is greatly diminished with more than 25 holdings. That knowledge deficit, along with allocating money away from our best ideas, makes it more difficult for us to produce attractive long-term returns in a risk averse way.

Further, we believe investors underestimate the differentiation in returns and valuations across companies comprising the market. To us, this variation provides an opportunity for concentrated portfolios to avoid the more overvalued and/or over-indebted sectors of the market….but only if rigorous selection criteria are met and you are disciplined about implementing your investment process.

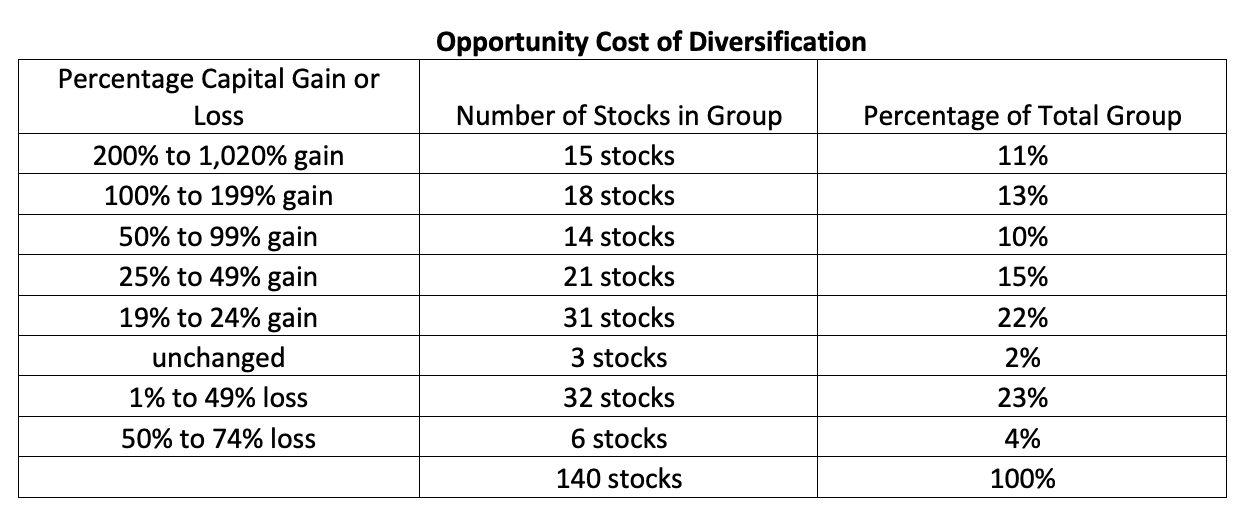

The aforementioned Philip Fisher, along with some of his Stanford University graduate business students, once conducted a study in which they calculated the roughly 5-year performance for a “random” set of 140 stocks (chosen solely based on the first letter in their names) from the New York Stock Exchange. Those performance results are shown in the table below. By comparison, the Dow Jones market averages gained 41% over the same time frame. (Common Stocks and Uncommon Profits first published in 1958)

It is clear that the return variance is significant across the 140 names. It Is also worth noting that 27% of the companies showed a loss during the period, while 24% of the group produced gains of at least 100%. It is certainly reasonable to believe that a focused investor, applying strict fundamental investment criteria, could at least sidestep most of the large declining stocks while picking up a few of the better performing ones.

Warren Buffett has described this blind faith in diversification as “protection against ignorance”; David Swenson who famously managed Yale’s endowment called it “failing conventionally”; and Peter Lynch referred to it as “deworsification.” We think of excess diversification as a high opportunity cost, which we believe is illustrated in the table above as well as by looking at the wide spread of returns among S&P 500 companies currently.

For example, in 2017, a great year for the S&P 500 Index with a 21.83% total return, Bespoke Investment Group found that the average return for the top 40 performers was 71.83% while the average return for the bottom 30 was a loss of 23.59%, obviously a wide spread. In no way will we ever match the performance numbers of the top 40 stocks or ever invest in the top performers while completely avoiding the bottom performers. We’re simply pointing out the spread in returns and the potential for a concentrated portfolio to outperform the index.

In our view, excess diversification can also dilute the knowledge and conviction in your investments, making you more prone to emotional mistakes during volatile market environments. Please feel free to contact us if you would like more information on our investment philosophy and performance. [email protected]

Mr. Nowell has forty years of experience in the finance business. Since founding South Atlantic Capital in 1991, he has been the sole portfolio manager of its Core Equity Composite, which has outperformed the S&P 500 since its inception on January 1, 1992, and ranks highly among its peers in performance and downside protection during that time period. Recently, he was named a top 10 performing manager by PSN Informa among Large Cap Value managers for the 3rd quarter of 2021 and was named a top 10 Manager of the Decade among all Large Cap Managers at year-end 2012. Previously, he was an Assistant Vice President at Bankers Trust Company in New York. His primary responsibility was arranging bank financing for leveraged buyouts led by Kohlberg Kravis and Roberts, Forstmann Little, and other leading private equity firms. During business school he interned with Merrill Lynch’s Capital Markets Group in New York. Later, he served as an Institutional Fixed-Income salesman with Carolina Securities/ Prudential Bache and worked with Fox, Graham, and Mintz Securities. He graduated from the University of North Carolina at Chapel Hill and received his M. B. A. from the Darden Graduate School of Business Administration at the University of Virginia.

Disclaimer- Past Performance is no guarantee of future results. Nothing in this article should be construed as investment advice of any kind. Consult your investment adviser before making any investment decision.

Industrial Building, Land On U.S. 421 Sells For Nearly $12M

Emma Dill

-

Apr 26, 2024

|

“My mission and my goal is to take my love of marine science, marine ecosystem and coastal ecosystems and bring that to students and teacher...

Baristas are incorporating craft cocktail techniques into show-stopping coffee drinks, and bartenders are mixing espresso and coffee liqueur...

W.R. Rayson is a family-owned manufacturer and converter of disposable paper products used in the dental, medical laboratory and beauty indu...

The 2024 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.